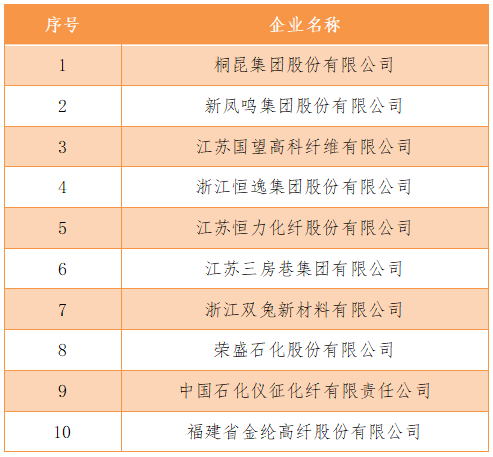

Recently, the China Chemical Fiber Industry Association released the “2017 China Chemical Fiber Industry Output Prediction List.” Among them, Tongkun Group, Xinfengming Group, Jiangsu Guowang Hi-Tech, Hengyi Group, and Jiangsu Hengli Chemical Fiber ranked among the top five in the list.

Preliminary list of China’s chemical fiber production in 2017 (top ten)

From the above output ranking, we can clearly see the size of the enterprise, and it can also reflect the production situation of the enterprise more truly. In addition, combined with recent industry hot news, it is not difficult to find that this year, whether it is the acquisition of bankrupt production capacity or the launch of new production capacity, it is actually the work of several polyester giants on the list!

This reminds me of a sentence: The market competition is fierce, and the reason why the strong remain strong is because they are not only richer and more famous than you, but they also work harder than you!

In recent years, chemical fiber leaders have adopted bottom-up chain expansion, and industrial concentration has been further strengthened. On the expansion path of various polyester companies, the editor below will introduce to you some typical representatives:

Speaking of expansion, the most impressive thing in 2017 is undoubtedly “Hengyi Speed”! Hengyi Group made three large-scale acquisitions in 2017, including Longteng, Hongjian, and Minghui, and restarted the three acquisition projects in a short period of time. Through these three acquisitions, Hengyi Group has increased its polyester production capacity by 1.4 million tons. At present, its total polyester filament production capacity is approximately 1.65 million tons, and its annual polyester production capacity is approximately 4.8 million tons, showing obvious scale advantages.

The pace of expansion continued in 2018. On the evening of March 2, Hengyi Petrochemical (000730) announced that the company planned to purchase 100% of the equity of Jiaxing Yipeng, 100% of Taicang Yifeng, Fulida Group and Xinghui Chemical Fiber Group held by Hengyi Group by issuing shares. It holds 100% equity of Shuangtu New Materials. After this transaction, Hengyi Petrochemical will increase its polyester fiber production capacity by 1.445 million tons per year. In addition, the 1.5 million tons Hainan bottle flakes project is expected to be put into operation in 2018, the 500,000 tons Shanghai polymer relocation project is expected to be put into operation in 2018, and Yikai (Haining Industrial Park) and Yifeng each have a production capacity plan of 1 million tons in 2019-2020. It is expected that by 2020, the total polyester production capacity of Hengyi Petrochemical and Group will reach 7 million tons.

While Hengyi Group is acting resolutely and demonstrating “Hengyi Speed”, other companies in the polyester industry are not idle either.

As one of the “leaders” in the domestic chemical fiber industry, Tongkun Group has also been making continuous moves recently. On February 23, the group announced that its Jiaxing Petrochemical FDY project with an annual output of 300,000 tons was put into operation. On the 26th, it issued two announcements announcing the launch of a new green intelligent fiber project with an annual output of 300,000 tons (Hengbang Phase 4). Heheng optimizes the construction of a differentiated POY technological transformation project with an annual fiber output of 300,000 tons. On March 8, the third phase of Hengbang’s 200,000-ton annual high-functional differentiated fiber technological transformation project was launched…

2017~2019 is a critical period for Tongkun Group to implement its three-year production expansion plan. According to the plan, the company’s polyester filament production capacity is expected to exceed 6 million tons per year by the end of 2019. According to statistics, from 2017 to 2019, domestic polyester filament yarn production will expand by a total of 5.1 million tons, of which Tongkun’s expansion will reach 2 million tons, accounting for 40%, making it the enterprise with the largest expansion.

In addition, Xin Fengming, who just entered the capital market in 2017, also said that 2018 was the year when the company “increased investment and co-constructed multiple projects” and achieved “three-year rebuilding” This is the year to tackle the grand goal of “A New Phoenix”. On March 10, the start-up ceremony of the CP11 unit of Sinopec Phase II was held. In addition to the Sinopec Phase II project, Zhongxin Phase II, the research institute project, the large boiler project, etc. will be completed and put into operation one after another. By then, Xinfengming’s production capacity will reach a new height.

Due to factors such as environmental protection restrictions and the inability of small companies to expand production, new production capacity in the industry in the future will mainly come from large companies. Among the new production capacity totaling 5.1 million tons from 2017 to 2019, Tongkun, Hengyi, and Sheng Leading companies such as Hong, Xinfengming and Rongsheng accounted for 75%, and almost all leading companies expanded production in 2018-19. It is worth noting that this also fully reflects the increasingly clear differentiation of the polyester filament industry, and the advantages of leading companies will become increasingly obvious.

A simple analysis of production capacity distribution shows that the concentration of polyester filament production capacity is further strengthening, and the future may be a situation where several leading companies divide the world. These companies are currently on the 2017 China chemical fiber industry production ranking list. Perhaps next year, it will be a completely different scene! </p